Return of Capital in Covered-Call ETFs: Tax Break or NAV Trap?

Return of capital in covered-call ETFs can be tax-efficient or destructive. Learn how Box 3, 19a-1 notices, NAV trends, and total return reveal the difference.

Every January, a wave of income investors opens their 1099-DIV and finds something odd: the biggest number on the form is sitting in Box 3, "Nondividend distributions." The fund paid a double-digit distribution rate all year, yet a huge slice of it apparently isn't taxable income at all. Some investors celebrate, convinced they've found a loophole. Others panic, convinced the fund is "just handing my own money back."

Both reactions miss the point. Return of capital (ROC) is an accounting label, not a verdict. In one fund it can be a deliberate tax-efficiency feature; in another it's the clearest warning sign that the payout is an illusion. The skill — and what this guide will teach you — is running the test that tells you which one you own.

Key takeaways

- Return of capital is not automatically bad.

- Tax-friendly ROC defers tax by reducing your cost basis.

- Destructive ROC shows up as a falling NAV, weak total return, and eventual payout cuts.

- A 19a-1 notice tells you the estimated source of a distribution; it does not prove the distribution is sustainable.

What Return of Capital Actually Is

A fund's distribution has to come from somewhere: net investment income (dividends and interest it collected), realized capital gains, or, when the payout exceeds the fund's earnings and profits for tax purposes, return of capital. That last slice is reported in Box 3 of your 1099-DIV as a nondividend distribution.

Here's the mechanical part that matters:

- ROC is not taxed in the year you receive it.

- Instead, it reduces your cost basis dollar-for-dollar.

- When you eventually sell, that lower basis produces a larger capital gain. If you held the shares for more than a year, that gain is generally long-term; if not, it can be short-term.

- If distributions ever push your basis all the way to zero, any further ROC is taxed as a capital gain in the year received — long-term or short-term depending on how long you've held the shares.

A quick example. Say you buy 100 shares of an option-income ETF at $50, and it pays $6 per share each year, classified entirely as ROC:

| Event | Cash received | Tax due that year | Cost basis (per share) |

|---|---|---|---|

| Purchase | — | — | $50.00 |

| Year 1 ROC | $600 | $0 | $44.00 |

| Year 2 ROC | $600 | $0 | $38.00 |

| Year 3 ROC | $600 | $0 | $32.00 |

| Sell at $50 | — | Tax on $18/share gain | — |

This assumes your basis stays above zero through the distribution years and that the shares are sold after a long-term holding period. The income wasn't tax-free; it was tax-deferred — and for a long-term holder, potentially rate-converted too.

Strategist's perspective: ROC turns "taxed now, at ordinary rates" into "taxed later" — and for shares held past the one-year mark, "taxed later at long-term capital-gains rates." That's two separate upgrades: timing, and often rate. Under current law, heirs also generally receive a stepped-up basis, which can turn deferral into something close to avoidance.

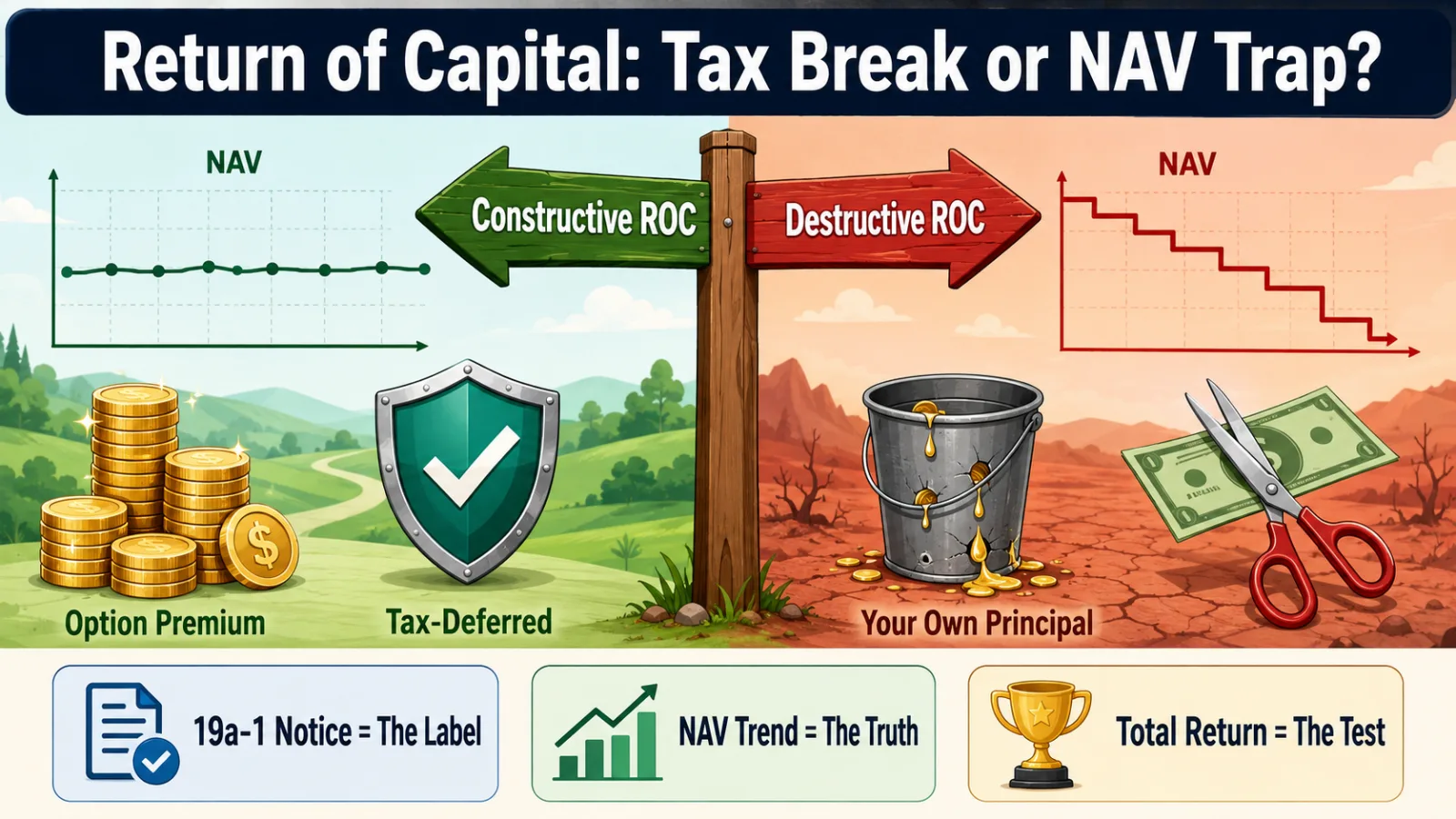

The Two Species of ROC: Constructive vs. Destructive

This is where most articles stop and most investors get burned. The tax form treats all ROC identically. The market does not. There are two very different animals wearing the same label.

Constructive ROC shows up in funds like SPYI and QQQI, which sell index options on the S&P 500 and Nasdaq-100. The cash they distribute comes from option premium, dividends, and gains, but the tax accounting — Section 1256 contracts with 60/40 treatment, plus active loss harvesting inside the fund — has historically led to a large share of distributions being classified as ROC. In a tax-managed fund like this, ROC may reflect tax accounting rather than economic liquidation — but that's a conclusion you should confirm against the NAV and total-return record, not assume. SPYI has traded since 2022; QQQI only launched in January 2024, so its long-term record is still being written.

Destructive ROC is the dark mirror. A fund earns, say, 6% from its strategy but insists on paying an 11% distribution rate. The difference has to come from somewhere, so the fund sells its own holdings and hands you the proceeds. Your "income" is partly your own principal coming back, minus fees, and the NAV grinds lower year after year. Each distribution is paid from a smaller asset base, so the dollar payout eventually shrinks too — the classic yield-trap death spiral.

The 19a-1 notice tells you the label. The NAV and total-return record tell you whether that label is harmless tax accounting or economic erosion.

The 60-Second NAV Test

Before buying any high-distribution fund whose payouts include ROC, run three checks:

Total return vs. distribution rate. Over a multi-year stretch, has total return (price change plus distributions) kept pace with the stated distribution rate? A fund paying 12% while delivering a 5% total return is liquidating itself in slow motion.

The long-term NAV trend. A flat or rising NAV alongside big distributions is the signature of constructive ROC. A staircase heading steadily down — across both up and down markets — is a serious warning sign, whatever the label says.

Distribution stability. Eroding funds are eventually forced to cut. A payout that has been trimmed repeatedly while the NAV falls is a confession.

You can run all three in about a minute on a comparison page — put the fund next to its peers and look at total return, not just the distribution rate. Start with the matchups income investors run most: JEPI vs SPYI, QQQI vs QYLD, JEPI vs JEPQ, or build your own in the ETF Comparator.

How to Read a 19a-1 Notice

When any part of a distribution comes from a source other than net investment income, Section 19(a) of the Investment Company Act requires the fund to tell you — that's the 19a-1 notice you'll find on the fund sponsor's website, usually near the distribution announcements.

What it shows, per distribution: the estimated portion drawn from net investment income, from realized gains, and from paid-in capital or other capital sources (the return-of-capital slice), plus the same breakdown year-to-date.

Three caveats that trip people up:

- The numbers are estimates. Funds are required to correct estimates that later prove materially inaccurate, and the figures can shift over the year.

- The final tax character arrives only on your 1099-DIV the following January. A distribution estimated at 90% ROC in March can be reclassified by year-end.

- A high ROC percentage is not, by itself, a warning. As we covered above, it can mean tax-managed option premium or it can mean self-liquidation. The 19a-1 tells you what the label is; the NAV test tells you what it means.

Where ROC Funds Belong: A Word on Account Placement

ROC's tax advantage — deferral plus potential rate conversion — only exists in a taxable account. Inside an IRA or 401(k), everything is already tax-deferred, so a ROC-heavy fund spends its best feature where it counts for little.

The flip side: funds built on equity-linked notes, like JEPI and JEPQ, have historically generated distributions that are mostly ordinary income with little ROC — the kind of income that tax-advantaged accounts shelter best. For many taxable investors, ROC-heavy 1256-option funds may be more tax-efficient in taxable accounts, while ordinary-income-heavy funds may be better candidates for tax-advantaged accounts. The right placement depends on your tax bracket, holding period, account mix, and goals.

One housekeeping note for taxable holders: your broker adjusts the basis on covered shares automatically, but keep an eye on positions you've held for many years. Once basis reaches zero, ROC stops being deferred and starts being taxed as capital gain in the year received.

A Field Guide to the Big Covered-Call Families

| ETF family | Income engine | Tax character to expect | Investor check |

|---|---|---|---|

| JEPI / JEPQ (JPMorgan) | Equity portfolio plus equity-linked notes | Often ordinary-income-heavy; verify annually | Tax drag in taxable accounts |

| SPYI / QQQI (NEOS) | Index options, often Section 1256 | Often ROC-heavy and tax-managed; verify the 19a-1 and 1099 | NAV and total-return test |

| QYLD (Global X) | Nasdaq-100 covered-call strategy | ROC has appeared in many years; distribution rate can differ sharply from SEC yield | Long-term NAV trend |

| Single-stock weekly option ETFs | Synthetic, single-name option exposure | Highly variable | NAV test is mandatory |

Distribution character changes year to year — always confirm against the fund's latest 19a-1 notice and tax documents. Note that ELN-based funds also carry counterparty and liquidity considerations described in their prospectuses.

Frequently Asked Questions

Is return of capital bad? Not inherently. ROC from option-income funds with stable NAVs can be a deliberate tax-efficiency feature. ROC from a fund whose NAV declines year after year means the payout is partly your own principal. Judge the NAV and total return, not the label.

How is return of capital taxed? It isn't, when received — it reduces your cost basis instead. You pay capital-gains tax on the difference when you sell (long-term or short-term depending on holding period), or immediately on any ROC received after your basis reaches zero.

Can ROC lower my taxes forever? Not usually. ROC generally defers tax by reducing basis. The tax bill can show up when you sell the shares, or sooner if your basis reaches zero.

Where do I find a fund's ROC percentage? Estimates appear in each 19a-1 notice on the sponsor's website; the final, official breakdown arrives on your 1099-DIV (Box 3) the following January.

Does ROC matter in an IRA? The tax advantage usually doesn't — inside an IRA or 401(k), ROC's basis-deferral benefit is mostly redundant. But the fund's economics — total return, volatility, NAV erosion, and payout stability — matter just as much there as anywhere else.

The Bottom Line

Return of capital is a tool, and like any tool it can build or demolish. The same three letters describe some of the most tax-efficient income strategies in the ETF market and some of its most damaging yield traps. Don't buy the label — buy the math: total return against distribution rate, and a NAV that can hold its ground while paying you.

Keep exploring:

- Why Your Fund's Yield Isn't Telling the Whole Story — the yield metrics that pair with this guide

- It's That Time of Year: Let's Talk Tax-Loss Harvesting — the same basis mechanics, used offensively

- ETF Comparator — run the 60-second NAV test on any funds side by side

- Dividend Tax Estimator — estimate the tax drag on your income stream

Tax laws and regulations are complex and subject to change. This guide is for educational purposes; always consult a qualified tax professional regarding your specific financial situation.