Where Should You Store Cash?

A practical look at Treasury bill ETFs, cash alternatives, and where investors may consider storing cash.

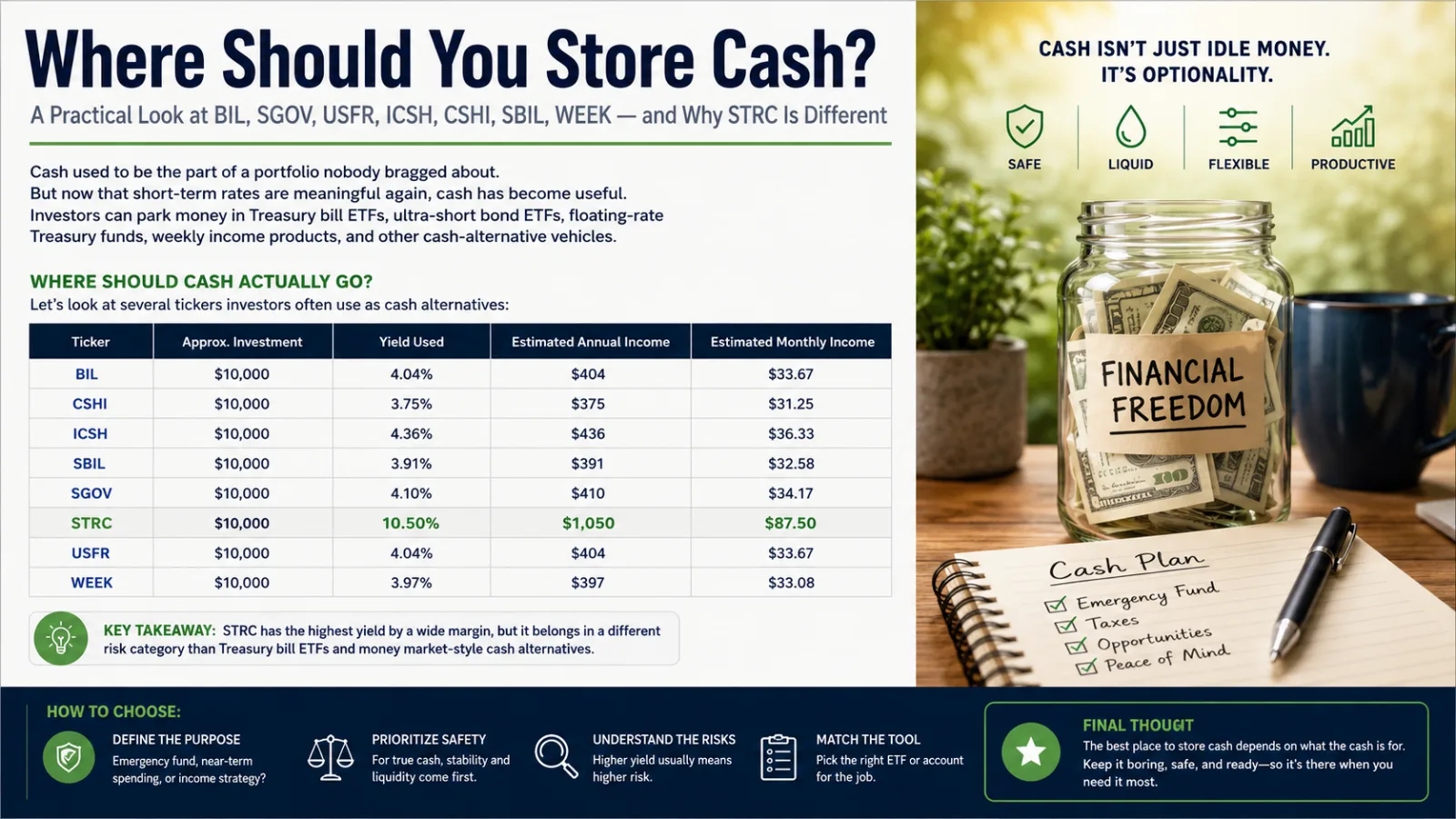

Where Should You Store Cash? A Practical Look at BIL, SGOV, USFR, ICSH, CSHI, SBIL, WEEK — and Why STRC Is Different

Cash used to be the part of a portfolio nobody bragged about.

It sat in a bank account, earned basically nothing, and quietly judged your spending habits from the corner. But now that short-term rates are meaningful again, cash has become useful. Investors can park money in Treasury bill ETFs, ultra-short bond ETFs, floating-rate Treasury funds, weekly income products, and other cash-alternative vehicles.

That creates a good problem:

Where should cash actually go?

Let’s look at several tickers investors often use as cash alternatives:

| Ticker | Approx. Investment | Yield Used | Estimated Annual Income | Estimated Monthly Income |

|---|---|---|---|---|

| BIL | $10,000 | 4.04% | $404 | $33.67 |

| CSHI | $10,000 | 3.75% | $375 | $31.25 |

| ICSH | $10,000 | 4.36% | $436 | $36.33 |

| SBIL | $10,000 | 3.91% | $391 | $32.58 |

| SGOV | $10,000 | 4.10% | $410 | $34.17 |

| STRC | $10,000 | 10.50% | $1,050 | $87.50 |

| USFR | $10,000 | 4.04% | $404 | $33.67 |

| WEEK | $10,000 | 3.97% | $397 | $33.08 |

At first glance, STRC looks like the obvious winner. It has the biggest yield by a mile.

But this is where investors need to slow down.

Cash is not supposed to be exciting. Cash is supposed to be stable, liquid, and boring enough to make a spreadsheet fall asleep.

First, Define What “Cash” Means

Not every “cash alternative” is the same.

For most investors, cash means money that should be:

- Stable

- Liquid

- Low-risk

- Easy to access

- Available for emergencies, taxes, opportunities, or near-term expenses

That means the goal is not to squeeze out every last drop of yield. The goal is to avoid taking unnecessary risk with money that is supposed to stay safe.

Cash is not supposed to win the Kentucky Derby. Cash is supposed to still be standing after the other horses started trading crypto options at 2 a.m.

Treasury Bill ETFs: The Cleanest Cash Parking Lot

The simplest cash alternatives in this group are Treasury bill-focused ETFs like BIL, SGOV, and WEEK.

These funds generally hold short-term U.S. Treasury bills or similar short-duration government securities. They are designed to provide income while keeping interest-rate risk relatively low.

They are not the same as FDIC-insured bank deposits, but they are often used by investors as brokerage-account cash alternatives.

For investors who want a clean, simple place to store cash inside a brokerage account, Treasury bill ETFs are usually one of the first categories to consider.

They are not designed to make you rich overnight. They are designed to keep your cash productive while you wait.

Basically, they are the financial equivalent of putting your money in a well-lit parking lot instead of leaving it behind a dumpster with a sticky note that says “please behave.”

BIL vs. SGOV vs. WEEK

Using the yields above:

| Ticker | Yield Used | Estimated Monthly Income on $10,000 |

|---|---|---|

| BIL | 4.04% | $33.67 |

| SGOV | 4.10% | $34.17 |

| WEEK | 3.97% | $33.08 |

The income difference between BIL and SGOV is small. SGOV has a slight yield edge in this example, but not enough to pretend we discovered electricity.

BIL is one of the classic short-term Treasury bill ETFs. It is simple, recognizable, and commonly used by investors looking for Treasury bill exposure.

SGOV is another popular Treasury bill ETF focused on very short-term Treasury exposure. In this example, it has a slightly higher yield than BIL.

WEEK is interesting because it focuses on weekly distributions. That may appeal to investors who like more frequent cash flow.

But investors should ask a simple question:

Do weekly payments actually matter, or do they just feel nice?

Sometimes weekly income is useful. Sometimes it is just dopamine with a ticker symbol.

If you are matching cash flow to weekly spending, weekly distributions may be convenient. But if your main goal is simply earning a competitive yield on idle cash, total return and safety matter more than how often the income hits the account.

USFR: Floating-Rate Treasury Exposure

USFR is a little different from a traditional Treasury bill ETF.

Instead of focusing only on regular short-term Treasury bills, it provides exposure to U.S. Treasury floating-rate notes. That means its income can adjust as short-term rates change.

Using your numbers:

| Ticker | Yield Used | Estimated Monthly Income on $10,000 |

|---|---|---|

| USFR | 4.04% | $33.67 |

USFR can make sense for investors who want Treasury exposure that responds to short-term rate movements.

In plain English: it is still Treasury-oriented, but the engine under the hood is different.

Floating-rate Treasury funds can be useful when short-term rates are elevated or changing. They may behave differently than fixed-rate Treasury bill ETFs because their payments adjust based on rate conditions.

That does not make USFR better or worse than BIL or SGOV. It just means investors should understand what they own.

Because “Treasury fund” is not one single thing. Finance loves making five versions of the same sandwich and then giving each one a ticker.

ICSH: Ultra-Short Bond Exposure, Not Pure Treasury Cash

ICSH is an ultra-short bond ETF. It aims to provide current income while keeping duration low.

But it is not the same thing as a pure Treasury bill ETF.

Ultra-short bond ETFs may hold investment-grade bonds, money market instruments, commercial paper, or other short-term fixed-income securities. That can potentially improve yield, but it may also introduce more credit exposure than Treasury-only products.

Using your numbers:

| Ticker | Yield Used | Estimated Monthly Income on $10,000 |

|---|---|---|

| ICSH | 4.36% | $36.33 |

That is the highest yield among the more traditional cash-alternative ETFs in your list, excluding STRC.

A simple way to think about it:

Treasury bill ETFs are more “cash parking.” Ultra-short bond ETFs are more “cash-adjacent income.”

Still conservative-ish. Just with a slightly sharper stapler.

For investors who want a little more yield and are comfortable with a little more complexity, ICSH may be worth comparing against Treasury bill ETFs.

But if the money absolutely cannot lose value, even temporarily, investors should be careful. Ultra-short bond funds can be conservative, but they are not always identical to cash.

That distinction matters.

Cash is supposed to be boring. Cash-adjacent income is allowed to be a little more interesting, but once things start wearing sunglasses indoors, check the risk section.

CSHI: Enhanced Cash Alternative

CSHI is an enhanced income cash-alternative ETF.

That means it is not just a plain Treasury bill product. It may use additional strategies, such as options, to try to enhance income.

Using your numbers:

| Ticker | Yield Used | Estimated Monthly Income on $10,000 |

|---|---|---|

| CSHI | 3.75% | $31.25 |

Interestingly, in this example, CSHI does not show the highest yield, even though it uses an enhanced strategy.

That is a good reminder: more complex does not always mean more income.

Complexity is not evil. But it does mean investors should read the label before drinking the financial smoothie.

CSHI may appeal to investors who want a cash-alternative strategy with more moving parts than a standard Treasury bill ETF. But investors should understand how the income is generated and what risks come with the strategy.

A good rule:

If a fund uses a strategy you cannot explain in one or two sentences, do not treat it like plain cash.

That does not mean avoid it. It means respect it.

SBIL: Money Market-Style ETF

SBIL is designed to behave more like a government money market-style ETF.

Using your numbers:

| Ticker | Yield Used | Estimated Monthly Income on $10,000 |

|---|---|---|

| SBIL | 3.91% | $32.58 |

SBIL may appeal to investors who want government money market characteristics in an ETF wrapper.

That said, investors should still compare it against traditional brokerage money market funds, Treasury bill ETFs, and bank savings accounts.

Sometimes the best answer is not another ETF.

Tragic, I know.

For investors who already have access to a competitive money market fund at their brokerage, SBIL may or may not be necessary. But for investors who prefer ETFs, it may be useful to have a money market-style option that trades like a fund inside a brokerage account.

As always, compare:

- Yield

- Expenses

- Liquidity

- Bid/ask spread

- Holdings

- Distribution schedule

- Tax treatment

Yes, that list is boring. That is how you know it belongs in a cash article.

STRC: Big Yield, Different Risk Category

Now let’s talk about STRC.

Using your numbers:

| Ticker | Yield Used | Estimated Monthly Income on $10,000 |

|---|---|---|

| STRC | 10.50% | $87.50 |

That is much higher than everything else in the list.

But STRC should not be lumped in with Treasury bill ETFs or money market-style cash alternatives.

The higher yield exists for a reason. Usually, that reason is not “free money because Wall Street forgot math.”

STRC may belong in an income bucket, but it should not be treated as true cash. It carries a different kind of risk than short-term Treasury products.

That does not automatically make it bad. It just means it is not the same thing.

Calling STRC “cash” would be like calling a chainsaw a butter knife because both can cut things.

Technically adjacent. Emotionally terrifying.

This is the most important lesson in the whole article:

A higher yield does not automatically mean a better cash alternative.

Sometimes higher yield means better opportunity.

Sometimes higher yield means more risk.

Sometimes higher yield means the market is screaming, “Please read the prospectus before touching this.”

STRC may be interesting for income investors, but it should be evaluated as an income security, not as a place to store emergency cash.

A Simple Way to Categorize These ETFs

| Category | Tickers | Best For |

|---|---|---|

| Treasury bill ETFs | BIL, SGOV, WEEK | Simple cash parking, emergency reserves, dry powder |

| Floating-rate Treasury ETF | USFR | Treasury exposure that adjusts with short-term rates |

| Ultra-short bond ETF | ICSH | Slightly higher income potential with more credit exposure |

| Enhanced cash alternative | CSHI | Investors comfortable with a more complex strategy |

| Money market-style ETF | SBIL | Investors who want government money market characteristics in ETF form |

| Higher-yield income security | STRC | Income investors, not true cash storage |

This framework helps avoid the biggest mistake investors make when comparing cash alternatives:

ranking everything by yield alone.

Yield matters, but it is only one part of the decision.

A Treasury bill ETF yielding around 4% and a higher-yielding income security are not automatically competing for the same job.

One may be trying to protect purchasing power on idle cash.

The other may be trying to generate income while taking more risk.

Same account. Different job description.

So Where Should Cash Go?

For true cash reserves, investors should generally prioritize:

- Safety

- Liquidity

- Stability

- Reasonable income

That usually points first toward:

- SGOV

- BIL

- USFR

- WEEK

- SBIL

For investors willing to accept more complexity or slightly different risks, ICSH and CSHI may be worth reviewing.

For investors chasing higher income, STRC stands out, but it belongs in a different category.

My Practical Ranking by Use Case

Best for Simple Treasury Cash Parking

SGOV or BIL

Both are straightforward Treasury-oriented choices. SGOV has a slight yield advantage in this example, while BIL is one of the classic names in the space.

These are good examples of funds investors may consider when they want cash-like Treasury exposure without manually buying individual Treasury bills.

Best for Weekly Income

WEEK

WEEK is useful if distribution frequency matters. Just make sure weekly income is actually useful to you, not just emotionally satisfying spreadsheet confetti.

Weekly distributions can feel great, especially for investors who like regular cash flow. But the distribution schedule should not override the bigger question: is this the right tool for the job?

Best for Floating-Rate Treasury Exposure

USFR

USFR may be attractive if you want Treasury exposure tied to floating-rate notes.

This may be useful in changing rate environments, but investors should understand that it is structured differently than a simple Treasury bill ETF.

Best for Slightly Higher Cash-Adjacent Yield

ICSH

ICSH offers a higher yield in this example, but investors should understand that it is not pure Treasury exposure.

It may fit investors who want a conservative income option but are willing to accept more credit exposure than a Treasury-only fund.

Best for Enhanced Strategy Investors

CSHI

CSHI may appeal to investors who want a cash-alternative strategy with more moving parts.

It may not be the simplest choice, but it may be interesting for investors who understand the strategy and are comfortable with the tradeoffs.

Not True Cash

STRC

STRC has the highest yield in this comparison, but it should not be treated like Treasury bill cash.

It may be an income idea. It may be worth researching. But it does not belong in the same mental bucket as Treasury bill ETFs or government money market-style cash alternatives.

The Big Mistake: Chasing Yield With Cash

The biggest mistake investors make with cash is treating the highest yield as the automatic winner.

That works fine until the “cash alternative” starts behaving less like cash and more like an income investment with feelings.

A cash allocation usually has a job:

- Emergency fund

- Tax money

- Down payment money

- Business reserves

- Dry powder for future investments

- Money waiting to be deployed

- Short-term spending needs

For those uses, stability matters more than squeezing out one more percent.

If your emergency fund drops at the exact moment you need it, that is not an emergency fund. That is a plot twist.

Cash Alternatives vs. Bank Accounts

ETF cash alternatives can be useful, but they are not identical to bank savings accounts.

A high-yield savings account may offer:

- FDIC insurance, within limits

- Simple access

- No market price movement

- Easy transfers

Treasury bill ETFs and similar funds may offer:

- Brokerage account convenience

- Competitive yields

- Daily market liquidity

- Potential tax advantages depending on holdings and state tax treatment

- Easy integration with an investment portfolio

Neither is automatically better. The right answer depends on the purpose of the cash.

For emergency cash, some investors may prefer bank savings accounts.

For brokerage cash waiting to be invested, Treasury bill ETFs may be more convenient.

For income-focused investors, ultra-short bond funds or enhanced strategies may be considered.

For yield hunters, higher-risk income products may be tempting — but they should not be confused with cash.

A Simple Cash Bucket Strategy

One practical approach is to split cash into different buckets.

| Cash Bucket | Possible Use | Potential Fit |

|---|---|---|

| Emergency cash | Immediate needs | Bank savings account or money market fund |

| Brokerage dry powder | Waiting to invest | SGOV, BIL, USFR, WEEK, SBIL |

| Conservative income cash-adjacent | Slightly higher income | ICSH, CSHI |

| Higher-yield income | Income strategy, not cash | STRC or other higher-risk income securities |

This helps investors avoid putting all “cash” into one mental category.

Because not all cash is the same.

Money needed next week should not be treated the same as money you are willing to risk for income.

The calendar matters.

So does the panic level.

Final Thought

The best place to store cash depends on what the cash is for.

If the money is for an emergency fund, taxes, a down payment, business reserves, or near-term spending, the priority should be stability.

That usually favors Treasury bill ETFs, floating-rate Treasury funds, money market-style products, or high-yield savings accounts.

If the money is part of an income strategy and you can tolerate more risk, then products like ICSH, CSHI, or STRC may be worth exploring.

But do not confuse yield with safety.

A 10% yield sitting next to a 4% yield is not automatically better. Sometimes it is better. Sometimes it is a warning label wearing a tuxedo.

Cash should be boring.

That is the job.

Disclaimer

This article is for educational and informational purposes only and is not financial advice.