Understanding the Wash Sale Rule: A Guide for New Investors

Introduction: Don't Let Taxes Complicate Your Investing Journey

Welcome to the world of investing! As you begin your journey, you'll encounter various rules and regulations. One of the most common for stock traders is the "wash sale rule." While it might sound intimidating, it's not a penalty. It's simply a tax regulation designed to ensure fairness, and it's easy to navigate once you understand the basics. This guide will break down the wash sale rule into simple, actionable concepts to help you invest with confidence.

1. What Exactly Is a Wash Sale?

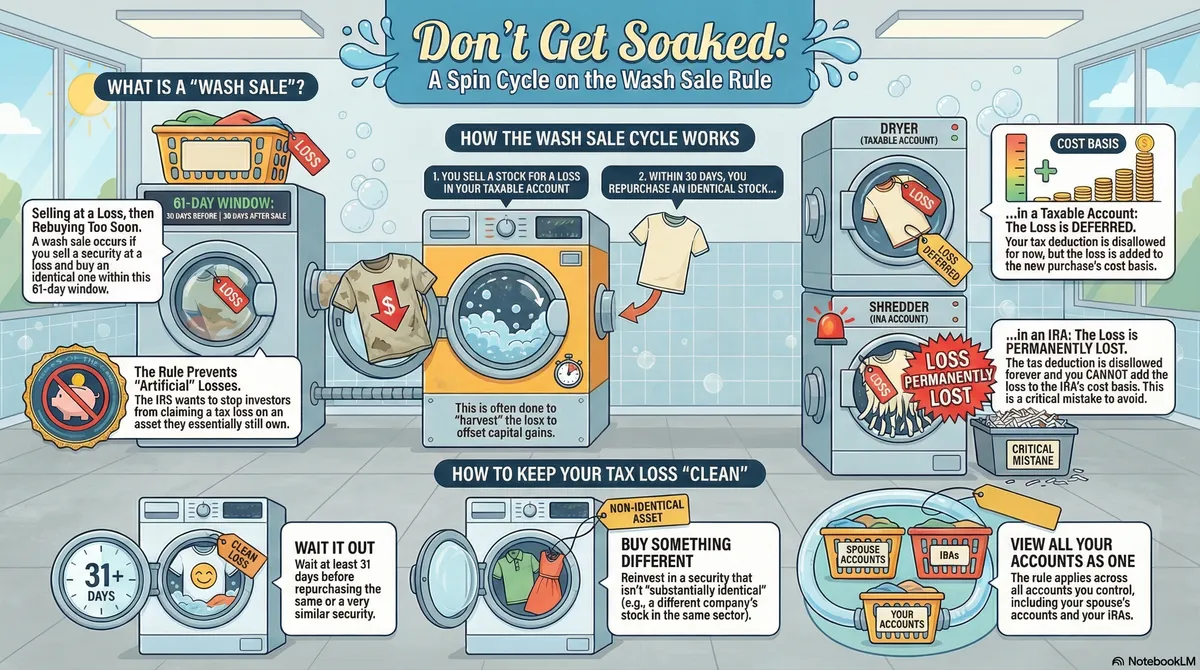

The wash sale rule is an IRS regulation designed to prevent investors from creating an artificial tax deduction. Specifically, it stops you from selling a security at a loss to claim a tax benefit, only to buy it (or something nearly identical) right back and maintain your position in the market.

1.1. The Core Rule in Simple Terms

A wash sale occurs when three specific conditions are met. Think of it as a simple checklist:

- You sell a security at a loss.

- You buy a "substantially identical" security.

- This purchase happens within a specific 61-day window.

1.2. Understanding the 61-Day Window

The timing of your repurchase is critical. The wash sale rule is triggered if you buy the substantially identical security within a 61-day period that includes:

- 30 days before the sale

- The day of the sale

- 30 days after the sale

If you repurchase a similar security at any point inside this 61-day timeframe, you have triggered a wash sale. Understanding these components naturally leads to the next question: what are the consequences of triggering the rule?

2. The Consequence of a Wash Sale: A Deferred, Not Denied, Loss

Triggering a wash sale isn't a penalty, and it's important to know that the rule is not designed to take your loss away forever. Instead, it simply postpones when you can claim the tax benefit.

2.1. How the Loss is Handled

The primary consequence is that you cannot deduct the loss from your taxes in the year of the sale. In simpler terms, the loss is disallowed for now.

2.2. The Magic of Basis Adjustment: An Example

When a wash sale occurs, the disallowed loss is not gone forever. Instead, it is added to the cost basis of the new, replacement shares you purchased. This adjustment effectively defers the tax benefit of the loss until you sell the new shares.

Let's walk through an example to see how this works.

| Step | Example Transaction |

|---|---|

| 1. Initial Purchase | You buy 100 shares of XYZ Corp. for $1,000. |

| 2. Sale at a Loss | You sell the 100 shares for $900, realizing a $100 loss. |

| 3. The Wash Sale Trigger | Within 30 days, you buy 100 shares of XYZ Corp. again for $950. |

| 4. The Consequence | Your $100 loss is disallowed for your current tax return. |

| 5. Basis Adjustment | The disallowed $100 loss is added to your new purchase price, making your cost basis $1,050 ($950 purchase price + $100 disallowed loss). |

The "so what?" of this adjustment is simple: when you eventually sell the new shares, your profit or loss will be calculated from this higher cost basis of $1,050. This will result in a smaller taxable gain or a larger deductible loss in the future, effectively giving you back the tax benefit of the original $100 loss.

While the consequences are straightforward, the definition of a wash sale hinges on a term that can be surprisingly ambiguous.

3. Demystifying "Substantially Identical" Securities

This is often the fuzziest part of the wash sale rule. The IRS has not provided a formal, all-encompassing definition, so investors rely on established guidelines and common sense.

3.1. The General "Rule of Thumb"

While there's no official definition, the commonly accepted guideline, especially for funds, is this: if two funds are designed to track the exact same market index, they are likely substantially identical.

3.2. Comparing Security Types

The table below provides clear guidance on what is generally considered identical versus not identical for tax-loss harvesting purposes.

| Security Type | Likely Substantially Identical | Likely NOT Substantially Identical |

|---|---|---|

| Company Stock | Shares of the same company. Options or convertible bonds of the same company. | Stock of a different company, even in the same industry. |

| ETFs & Mutual Funds | Two S&P 500 index funds from different providers. | An S&P 500 index fund and a total stock market index fund. |

It's helpful to remember this note, referenced from former IRS Publication 564:

"Ordinarily, shares issued by one mutual fund are not considered to be substantially identical to shares issued by another mutual fund."

Beyond the core definitions, it's crucial to understand how broadly the rule applies to your financial life.

4. Two Critical Details to Remember

Keep the following points in mind, as they define the broad reach of the wash sale rule.

- The rule applies across all your accounts. The IRS looks at your transactions across all of your accounts. This means you cannot get around the rule by selling a stock at a loss in your taxable brokerage account and then buying it back in your IRA within the 61-day window. Such a transaction is still a wash sale.

- The rule can apply to your spouse. The IRS also considers purchases made by your spouse as your own for the purposes of this rule. You cannot sell a stock for a loss and have your spouse buy back the same stock in their account within the 61-day window without triggering a wash sale.

5. Key Takeaways for the Smart Investor

As you manage your investments, distilling the wash sale rule into a few core principles will help you make savvy, tax-aware decisions.

- The wash sale rule defers your loss, it doesn't erase it. Remember that the disallowed loss is added to the cost basis of your new investment. This preserves its value, allowing you to claim that tax benefit when you eventually sell the replacement security.

- "Substantially identical" is about function, not just name. For ETFs and mutual funds, the key question is whether they track the same specific index. When in doubt, the safest path is to choose a replacement investment with a different underlying index or objective. Use the ETF Comparator to evaluate how two funds differ before making the swap.

- When unsure, seek guidance. Tax laws and regulations are complex and subject to change. This guide is for educational purposes; you should always consult a qualified tax professional regarding your specific financial situation.

Keep Exploring

- Tax-Loss Harvesting Guide — The companion strategy that makes the wash sale rule relevant

- Dividend Tax Estimator — Estimate your federal and state dividend tax liability

- ETF Comparator — Compare funds side by side to find non-identical replacements

- ETF Screener — Search for alternative funds by strategy, sector, or yield

- SEC Yield vs. Distribution Yield — Understand what you're actually earning before you sell