Autocallable ETFs Explained: High Income for a Capped Upside

Autocallable ETFs wrap Wall Street's structured notes in an exchange-traded package. How the barriers work, where the income comes from, and the risks.

Open the screener, sort by distribution rate, and the funds at the very top are increasingly a new breed: an ETF advertising a 40%, 50%, even 60% "distribution rate" tied to a single stock like PLTR or MSTR. They aren't covered-call funds. They aren't leveraged. They're autocallable ETFs — and they package one of Wall Street's most popular structured products into something you can buy one share of.

Autocallables have been sold to private-bank clients for decades, usually as six-figure structured notes. Wrapping them in an ETF is brand new — the first single-stock autocallable ETFs launched in early 2026. This guide explains what the structure actually is, where that eye-catching income comes from, and the trade-offs hiding behind the headline rate.

Key takeaways

- An autocallable pays a contingent coupon as long as the underlying stays above a downside "barrier," and redeems early ("auto-calls") if the underlying is flat to higher on an observation date.

- You trade away the upside: your best case is collecting coupons, not capturing the stock's rally.

- The downside protection is conditional, not a buffer — breach the barrier at maturity and you take the underlying's full loss from day one.

- The ETF wrapper fixes the classic structured-note problems (high minimums, illiquidity, single-bank and single-date concentration) by holding a laddered basket you can trade intraday.

- A high distribution rate is a contingent coupon, not a yield — judge these funds on total return and NAV, like any high-payout fund.

What an Autocallable Actually Is

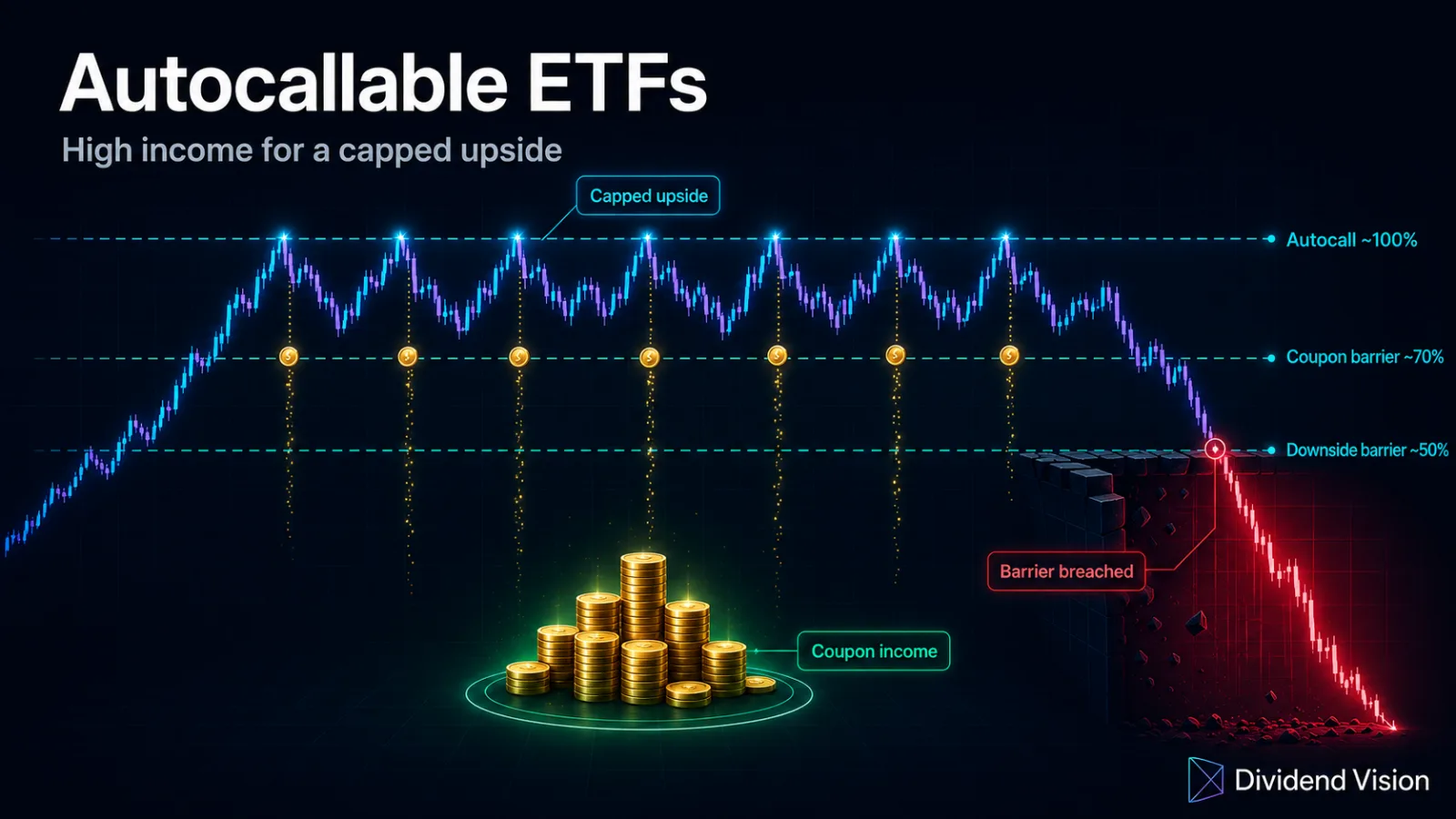

An autocallable is a structured product linked to an underlying — a single stock (PLTR, TSLA, NVDA, COIN, MSTR, HOOD) or a broad index (the S&P 500, the Nasdaq-100). At launch, the issuer records the underlying's starting level and sets three reference points off it. Then, on a recurring schedule of observation dates (often monthly or quarterly), the structure checks where the underlying is trading and decides whether to pay you, redeem early, or keep running.

Those three reference points are the whole game.

The Three Barriers That Define the Trade

| Reference point | Typical level | What it does |

|---|---|---|

| Coupon barrier | ~70% of the starting price | On each observation date, if the underlying is at or above this level, you're paid a coupon. Below it, that period's coupon is skipped — though some structures have a "memory" feature that pays missed coupons later if the level recovers. |

| Autocall trigger | ~100% of the starting price | If the underlying is at or above its starting level on an observation date, the note is "called" — redeemed early at par plus the coupon. The trade ends and the cash rolls into a new autocallable. |

| Downside / maturity barrier | ~50% of the starting price | Only matters if the note is never called. At maturity, if the underlying is above this barrier you get your principal back; if it closes below, the protection vanishes and you absorb the underlying's full loss from its starting level. |

(Levels are illustrative — every fund and every note sets its own.)

Three Ways It Can Play Out

Take a single-stock autocallable on a $100 stock with a 70% coupon barrier, a 100% autocall trigger, and a 50% downside barrier:

- The stock rises or holds (≥ $100 on an observation date). It auto-calls. You collect the coupon and your principal back — but you do not get the stock's gain. If it ran to $130, that $30 was never yours; you got the coupon. The cash rolls into a fresh autocallable.

- The stock drifts sideways or dips, but stays above $70. No early call, but you keep banking coupons in every period the stock sits above the coupon barrier. This is the structure's sweet spot: a flat-to-choppy stock that pays you to wait.

- The stock falls hard and finishes below $50 at maturity. The barrier is breached. The conditional protection disappears and you take the full loss from $100 — the same as owning the stock outright from the top, minus whatever coupons you collected along the way.

That asymmetry is the entire story: capped upside in exchange for income and a conditional cushion. Autocallables shine in flat, sideways, or mildly volatile markets, and lose their appeal in a runaway bull market (you miss the rally) or a crash (the barrier breaks).

Why Put It in an ETF?

Bought individually, a structured note has well-known problems: a high minimum (often thousands of dollars per note), little or no liquidity before maturity, the credit risk of the single bank that issued it, and "all-or-nothing" timing tied to one set of observation dates. The ETF wrapper is built to neutralize each of those:

- Laddering. Instead of one note, the fund holds dozens of autocallables with staggered start and maturity dates — Calamos's CAIE, for instance, runs more than 50 at a time. Staggering smooths the income and spreads out the "what was the level on that date" path risk.

- Liquidity. It trades intraday like any ETF. No waiting years for a single note to call or mature.

- One-share minimum. A strategy that used to require five or six figures now costs the price of one share.

- Diversified, professionally rolled exposure. When an autocallable calls or matures, the manager reinvests into a new one automatically, spreading exposure across counterparties and entry points instead of one bank on one day.

A fair caveat: the wrapper reduces but doesn't erase counterparty and structural risk, and it adds a management fee — roughly 0.74% on the index funds and about 1.07% on the single-stock funds currently on the market. You're paying for the packaging and the active rolling.

The Autocallable ETFs on Dividend Vision

The category went from zero to a couple of dozen funds in under a year. You can browse the live list — with current distribution rates, AUM, and expense ratios — on the Autocallable tag page. The main approaches:

| Approach | Examples | What's under the hood |

|---|---|---|

| Single-stock income | GraniteShares ANV (NVDA), TLA (TSLA), PLA (PLTR), ATC (COIN), MSR (MSTR), AHD (HOOD) | A laddered book of autocallables on one high-volatility stock. The most volatile names throw off the highest — and least predictable — contingent coupons. |

| Broad-index income | Calamos CAIE (US large cap) and CAIQ (Nasdaq-100); VegaShares VAIE; REX ATCL; TrueShares PAYH | Autocallables on an index rather than a single name — lower headline rates, but a far less fragile downside barrier. |

| Growth / compounding | Calamos CAGE | Reinvests the structure's return for tax-deferred growth instead of paying it out. |

| Laddered barrier funds | First Trust ACYN; Innovator ACEI and ACII | Defined-outcome-style autocallable barrier strategies from the buffer-ETF crowd. |

Single-stock funds have shown headline distribution rates from the high teens to north of 60%; the broad-index funds tend to land in the low-to-high teens. The pattern is intuitive — more underlying volatility buys a bigger contingent coupon and a more fragile barrier.

That Huge "Distribution Rate" Is a Contingent Coupon, Not a Yield

Here is where autocallable ETFs meet the same scrutiny as every other high-payout fund. A 50% distribution rate on a single-stock autocallable ETF is not a 50% yield in any conventional sense:

- It's contingent. Coupons are only paid when the underlying is above the coupon barrier on the observation date. A sharp drop can switch the income off.

- The upside is capped. Your total return can't run away the way the stock can — you're collecting coupons, not compounding the equity.

- Part of it can be return of capital. As with covered-call funds, a slice of the distribution may be classified as return of capital, which lowers your cost basis instead of handing you fresh income. (See Return of Capital in Covered-Call ETFs for the full mechanics.)

The honest way to evaluate one is the same 60-second test you'd run on any double-digit payer: put total return (price change plus distributions) next to the distribution rate, and watch the NAV over time. A fund paying a 40% rate while its NAV grinds steadily lower is returning your own capital, not generating 40% of income. Our SEC yield vs. distribution yield guide walks through why the headline number so often overstates the economics.

Who They're For

Autocallable ETFs are a tactical income tool, not a core holding. They make the most sense for an investor who:

- Wants equity-linked income but expects a flat, sideways, or only mildly rising market;

- Is willing to give up the big upside in exchange for a coupon and a partial cushion;

- Understands that the "protection" is conditional and can disappear in a deep drawdown;

- Sizes the position accordingly — especially the single-stock funds, which stack concentrated, idiosyncratic risk on top of the structure's own complexity.

Because the whole category launched in 2025–2026, none of these funds has a multi-year, full-cycle track record yet. That alone is reason to keep positions modest until you've seen how they behave through a real drawdown.

Frequently Asked Questions

Are autocallable ETFs safe? They're lower-risk than owning the underlying stock outright only as long as the downside barrier holds. Breach it at maturity and you take the full loss from the starting level. Think of them as a way to reshape an equity's payoff, not as a capital-preservation vehicle.

What does "autocall" mean? The structure automatically redeems early — at par plus the coupon — if the underlying is at or above its starting level on a scheduled observation date. The fund then rolls the proceeds into a new autocallable.

Why are the distribution rates so high? The coupon is the price the structure pays for taking on the underlying's volatility and capping your upside. The more volatile the underlying (a single momentum stock vs. a broad index), the larger — and less reliable — the coupon.

Do I get the stock's gains? No. Your best outcome is collecting coupons and getting your principal back. If the underlying doubles, the autocallable still just pays its coupon and usually calls away.

Index vs. single-stock — what's the difference? A single-stock autocallable can have its barrier broken by one company's bad week. An index autocallable spreads that risk across hundreds of names, which is why its barrier is much harder to breach and its coupon correspondingly smaller.

The Bottom Line

Autocallable ETFs democratize a strategy that used to live behind a private-banking minimum, turning a complex, illiquid structured note into a one-share, exchange-traded basket. Used in the right market — flat to mildly volatile — they can pay a generous, equity-linked income. But the structure is a genuine trade: you hand over the upside and accept a cushion that only holds above the barrier. Don't read the distribution rate as a yield. Read the prospectus, watch the NAV, and start small.

Browse every autocallable ETF we track — with live distribution rates, AUM, and expense ratios — on the Autocallable tag page.

Keep Exploring

- Return of Capital in Covered-Call ETFs: Tax Break or NAV Trap? — why a big payout can include your own principal

- Why Your Fund's Yield Isn't Telling the Whole Story — distribution rate vs. SEC yield vs. total return

- Autocallable ETFs on Dividend Vision — the full, live list

Autocallable ETFs are complex products that can lose value, including in ways that differ from owning the underlying asset. This article is for educational purposes only and is not investment advice; review each fund's prospectus and consult a qualified professional about your situation.